Forward Note - 20260329

On the verge of total collapse?

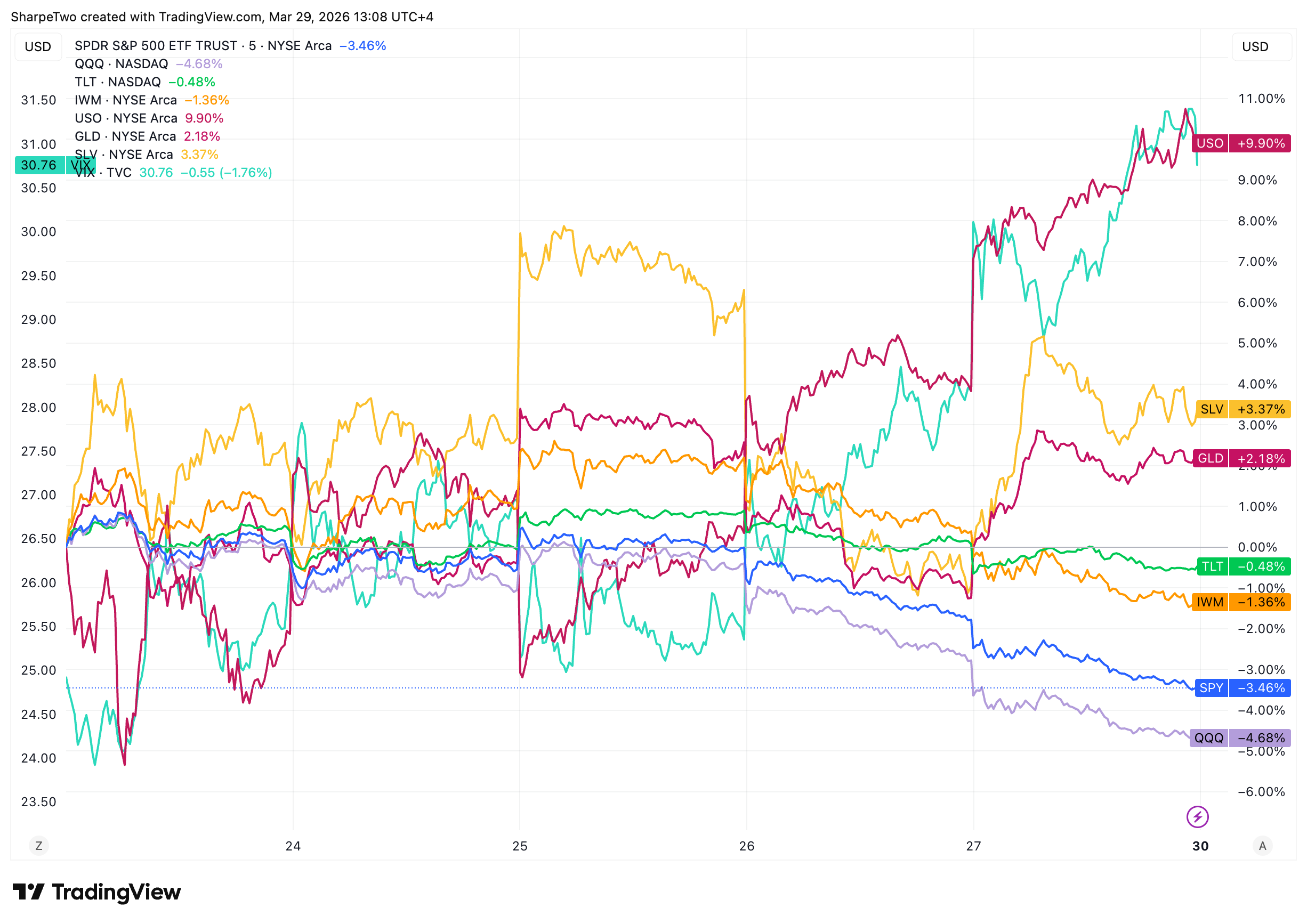

Almost like a repeat of a year ago, the market seems to be on the verge of total collapse. US equities are printing six-month lows, with the S&P 500 losing 3.5% this week and the Nasdaq more than 4%, the bulk of the loss happening at the back of the week on Thursday and Friday. The VIX closed above 30 at 31.4.

It was deemed to happen after three weeks getting really comfortable above 25 with no evident sign of immediate resolution of the pressing geopolitical matter. We heard on Monday that President Trump was apparently discussing with the Iranians, that the discussions were productive and led him to delay his attacks on key energy infrastructure of the country, and in general the US strikes. In return, we heard from the Iranians that President Trump must be discussing with himself as there was no formal contact between anyone, and that for now the Strait of Hormuz would remain closed and they would continue to defend themselves against the Israeli strikes, which despite President Trump's announcement on Monday, insisted they would continue.

Needless to say, a gigantic mess and four weeks in, no one knows exactly how this thing ends. Hopefully and obviously, every party ends up signing a well needed peace plan, but the alternative... becomes slightly concerning. And therefore, investors have decided that it was now time to go run for safety while waiting for more tangible answers.

And why would it be otherwise? The OECD has already warned that inflation was going to rise significantly in the US to reach 4.2%, making the job of the next Fed Chairman increasingly more complicated. And while the US President was bragging on Friday that he was getting bored (sic) with the war in Iran and that it did not really matter to him as the US had oil of their own (sic), the Philippines, which declared a state of emergency as they have now exhausted their oil reserves, will appreciate these comments. We are certain of it.

In such a context, and not different from the last four weeks: the goal is to survive the storm and not try to be a hero. In particular over the last month or so, US equities were fairly behaving despite the increasing realized volatility. But it looks like that ship may have sailed: the relative sell off of the last few days will surely have challenged the position of those who wanted to stay delta neutral. Stocks are now down 8% for the month of March alone and while in the grand scheme of things this may be just another blip, it will start to weigh on whoever was over-leveraged or not properly hedged.

And at 19% realized volatility over the last 30 days, the likelihood to see violent moves up or down has drastically increased. We wrote a similar analysis at the heart of the lazy summer (Forward Note, July 2025) pointing that at 8% realized volatility and VIX6M at 19, the market was bracing itself for maybe one bad day (characterized by a move above 1%) a month over the next six months. These odds significantly increase with the current market conditions: the probability of seeing a single day move above 2% with realized volatility close to 20% is around 11% on any given day, and over the course of a month, there is a 92% chance you will see at least one such day. And if you take the market expectations of volatility instead of what we just measured (so yes, the VIX) at 30%, that probability becomes a virtual certainty with about six such days expected every month.

Under these same market assumptions, the probability of seeing a move of 5% or more is now around 16% over the next month under Gaussian assumptions, and closer to 35% when you account for the fat tails that equity markets actually exhibit.

Essentially, if your book is not equipped to sustain one or two of these big moves in a row, or even more, you need to do whatever is necessary right now. It is obviously harder for the author of a newsletter to talk about how to hedge risk as the situation, as well as risk tolerance (but more importantly perception) of risk are rather different from one individual to the next. That said, based on some of the questions in our Discord this week, here are a few concrete steps:

At VIX 30, puts are really expensive and buying them should only be a last resort. In fact, if your book was balanced, you could and should be selling these tails and hedging them with longer dated ones, to recreate some skew swap structure. Selling puts naked in that uncertainty is unwise at best, stupid at worst (casual reminder: you can still do something stupid and be lucky. Do not mix it up with it being a strategy).

The cheaper hedge in these circumstances is often... to sell some shares. That is it, adding some good old negative delta with no optionality at all, and wait. The downside is evident: if the market rebounds violently, you will blame yourself for selling these futures. But the goal is to be delta neutral at best, or at least control your delta exposure to keep it to what you want, not to a level where it can obliterate your account.

If you have a problem with volatility expanding to uncomfortable levels, your best bet at the moment is to buy some short term or mid VIX futures. With the same caveat as the short delta: if there is good news tomorrow, they will lose a lot of value real soon real fast, and you will blame yourself for not having held on a little longer. The goal is to do risk management and control your exposure. Not to be a hero. Once again, assess your situation thoroughly and pick your side.

That is for playing defense. But in situations like this, if you had done your homework, there are some really interesting situations to go after. We mentioned the very expensive tails that can currently be swapped for longer dated ones in US equities, and one can consider some similar trades in asset classes that should not be impacted as much. Top of mind right now are rates; while the risk of inflation is real and probably already trickling down to the economy, it is not a systematic problem just yet, and it is likely that the market is getting a little ahead of itself.

And how about oil? A few weeks back we were telling you that a good trade could be to sell the very expensive USO calls and buy some ES puts with the proceeds. That position should be in the green with the moves this week, but should you do more of it? We are torn: the premise of that trade is that a quick resolution would occur. It must, right? But what if it does not, and the Middle East becomes a second hot geopolitical theater? That is a real possibility the market is slowly getting warmed to and we would not necessarily encourage taking that trade. Instead, one could consider selling the really expensive calls in the energy sector at the moment, and maybe... buy a few calls from the beaten down tech stocks.

Yes AI, yes inflation, yes problems all over the world. But: are you reading this note on a piece of paper, or a formidable piece of technology...?

In other news

$580 million of oil futures sold in a two-minute window on Monday morning, fifteen minutes before the President posted on Truth Social that talks with Iran were "productive." 6,200 contracts against a normal volume of 700 for that time slot. Nine times the average. Someone, somewhere, knew.

What is fascinating from a market standpoint is not even the potential insider trading itself (though the CFTC seems profoundly uninterested in finding out). It is that whoever had the information chose to sell oil. Think about it: if you know that there are productive talks with Iran, the logical next step is the Strait of Hormuz reopening. And if the Strait reopens, a massive amount of supply that has been stuck for weeks floods the market. Oil does not just dip on the announcement, it could crater on the follow-through.

So the trade was not just front-running a headline, it was pricing in the second-order consequence that most of the market had not even started thinking about. Is the position still on right now? Hard to tell. Although early in the week, some suspicious account were betting heavily on Polymarket that a cease fire would be reach by the end of March.

Thank you for staying with us until the end; as usual, here are two great reads from last week:

Ever heard of the theory of entenglement? Probably not and it is okay. Yet scientists at the University of the Witwatersrand have discovered that entangled photons contain hidden topological structures reaching 48 dimensions, with more than 17,000 distinct signatures. Using nothing more than orbital angular momentum of light, they have essentially found a vast new alphabet for quantum information. The implications for quantum computing are, to say the least, significant.

A developer spending $2,000 a month on Claude API tokens decided to build his own AI infrastructure instead: a Mac Studio M3 Ultra and dual NVIDIA DGX Sparks, running a 397 billion parameter model entirely offline. Ten-month break-even and then zero-cost inference forever. A beautifully honest account of the economics of self-hosted AI.

That is it for us this week, we wish you a much quieter week, and as usual, happy trading.

Ksander