Forward Note - 20260322

Wisdom of the crowd

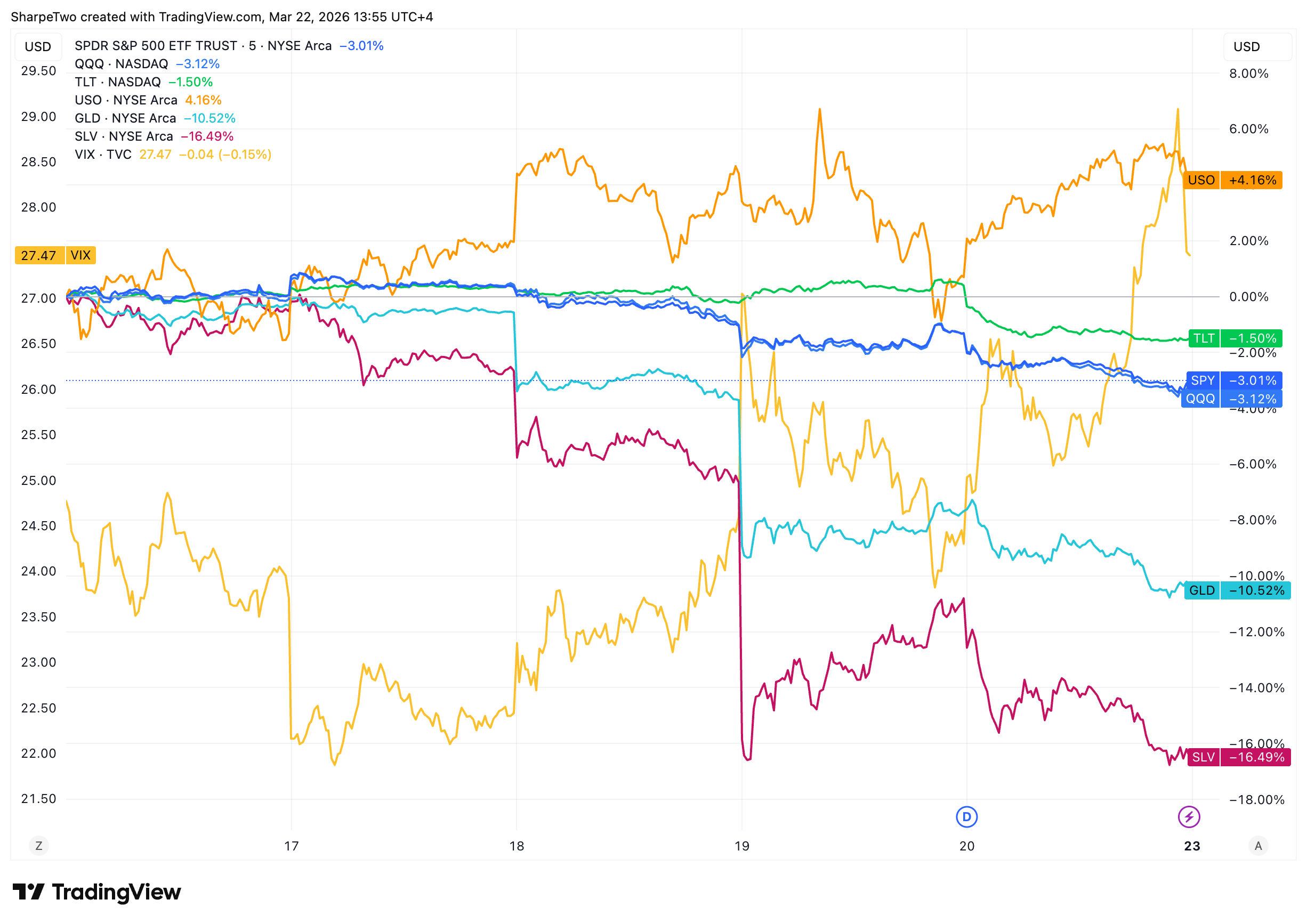

Third week of the conflict between Iran and the US/Israel coalition, and the market is now slowly waking up to the possibility of consequences going much further than what was envisioned early on. The S&P 500 and the Nasdaq both lost 3%, as the prospect of higher inflation triggered by higher oil prices is trickling down.

The VIX is still firmly anchored above the 25 handle and closed at 27.47, flirting with the 30 handle on Friday, as the market was going through triple witching and participants were looking for hedges in case things got heated again over the weekend.

And why would it be otherwise? Contradicting messages have been the only norm over the last few days. One day we hear that the “war would end much sooner” than people think, as laid out by Netanyahu after announcing that Iran’s nuclear program has been completely destroyed, but shortly followed by the announcement of more troops sent to the region that should arrive over the next few weeks.

The same back and forth between good and bad news continued over the weekend: while Donald Trump explained on truth social that he was considering winding down military operations in Iran, we learnt this morning that he gave Iran 48 hours to reopen the Strait of Hormuz or else he would target its power plants.

It’s too sunny of a Sunday to wonder too much how the market will react, yet, one doesn’t need a PhD in geopolitics to understand that the VIX isn’t exactly going to deflate from its current level.

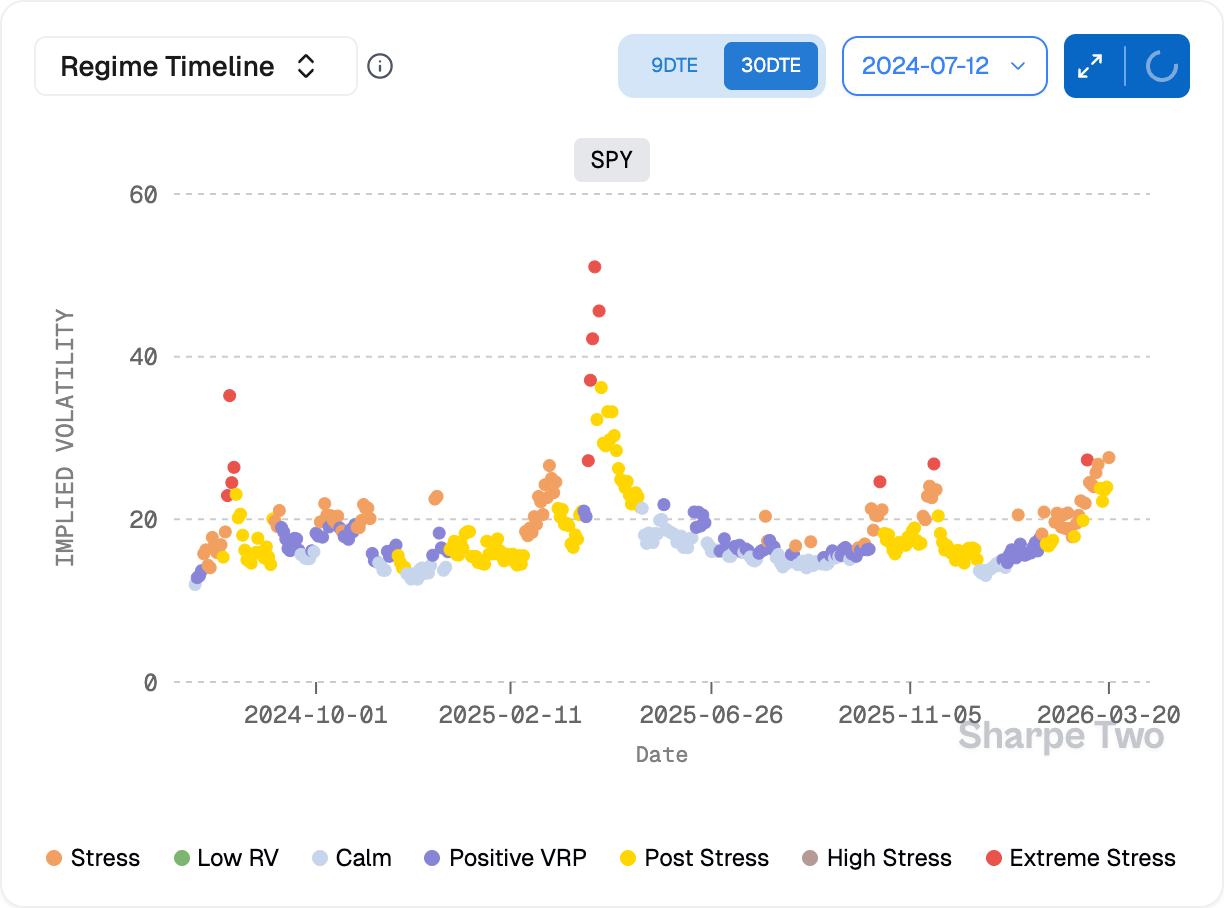

And while until now, realized volatility has failed to pick up meaningfully, the sessions post FOMC have been quite rocky and may signal a shift in investor sentiment.

We close the week at 17.25 over the last 30 days, levels we haven’t seen since the post-tariff war last year. And if you feel a little uneasy at these levels, you can look back at some of those sessions in March 2025 where realized volatility was comfortably above 20 and where these seas were not particularly fun to navigate.

The big difference this time is that the market still overpays significantly for the risk currently realized. Or … does it? We tend to stay clear from speculation and too much macro commentary. Yet, if we draw some parallels with last year, we ought to draw them all the way. In late March 2025, we knew some tariff announcements were on the way, and while no one in their right mind was thinking about the magnitude they would reach, the world was not going through a major regional conflict: China and the US fighting over tariffs is infinitely safer and more predictable than drones flying over Qatar, the Emirates and Saudi, the Strait of Hormuz close and with limited information as to when and how all of this stop.

So if you ask us, every extra day that passes now makes the premium more and more justifiable. By definition, when a situation becomes abnormal this is where we like to pounce, but when the abnormal normalizes as time passes… what are you supposed to do? Revise the original thesis, readjust your prior and wait for new information.

One thing is for certain at that stage: we are at a level of implied volatility where either things break and a volatility spike occurs and with it the uncertainty in the marketplace comes down, or the situation diffuses from there. We would be the first one to hope for a rapid de-escalation (even though 99.5% of the missiles are getting intercepted, a safer approach would be 0% of missiles thrown in our direction) but hope is rarely a rational strategy.

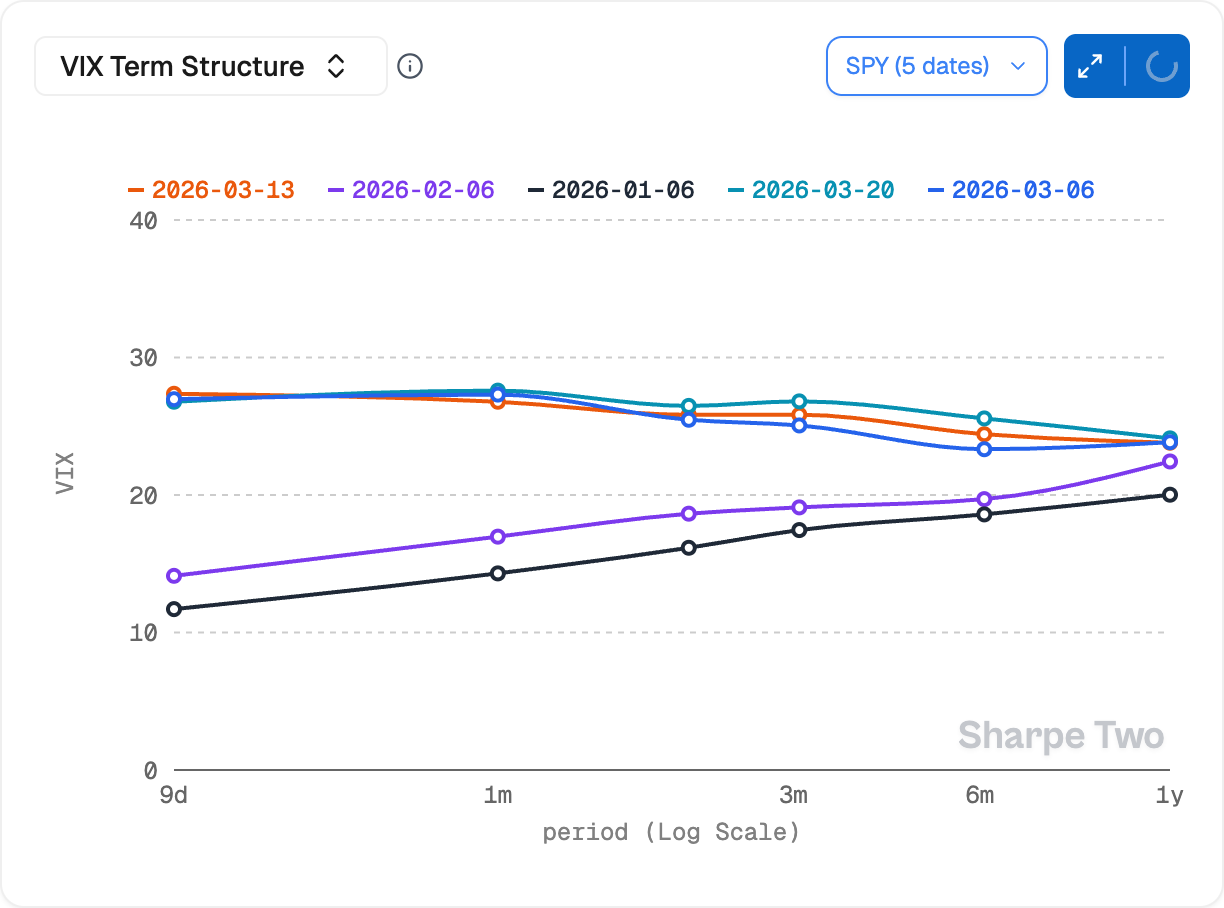

The term structure has been flattish with some early backwardation tendencies, especially as people look for hedges over the weekend. This highlights something important: nobody knows, and more people than not are ready for the unexpected. We often wrote in normal/low volatility regimes that betting on a brisk VIX expansion from 16 (good old days…) signalling that no one is buying insurance, may be really unwise when everything is nicely in contango. One has to make the same reasoning in the current circumstances: betting on a prompt resolution may become a little presumptuous when the entire marketplace is hedged to the teeth. It’s like seeing a storm brewing outside, people entirely dressed for unfriendly weather, and still deciding to get out as if it was August 3rd in the south of Italy. One has to respect the wisdom of the crowd.

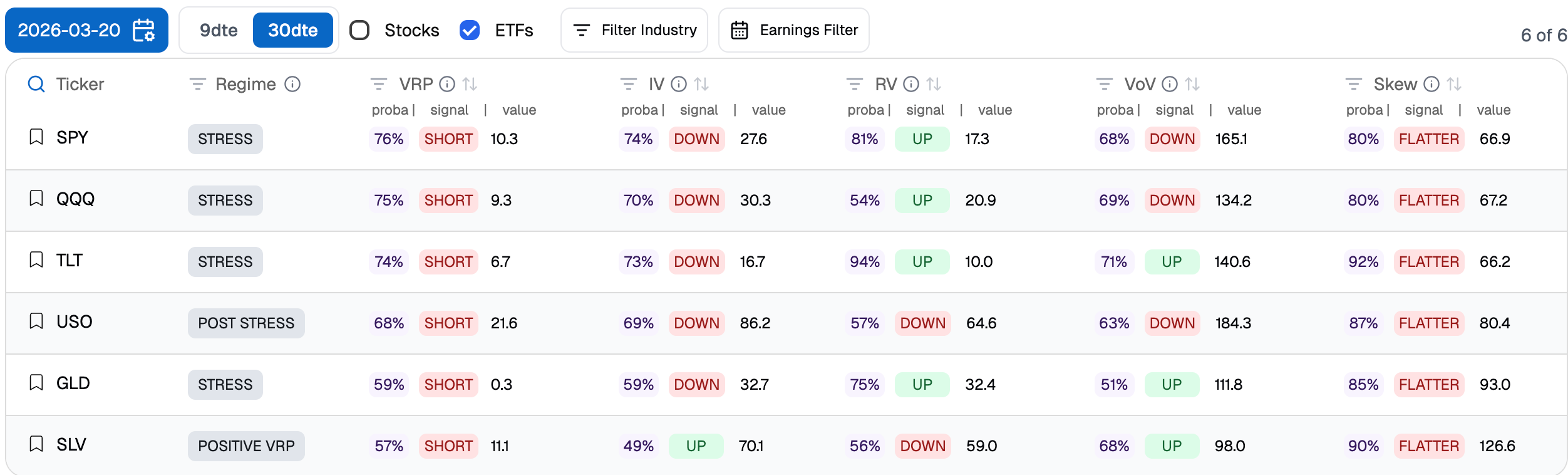

Therefore, adding more risk here? Sure, if you are sure that a sudden move to VIX 50 would only be mildly annoying. At the end of the day, 10 points VRP is still a decent trade to take (you had 0 points VRP and even negative VRP in the antechamber of the tariff war last year) but as we explained above, it can quickly come back to bite you.

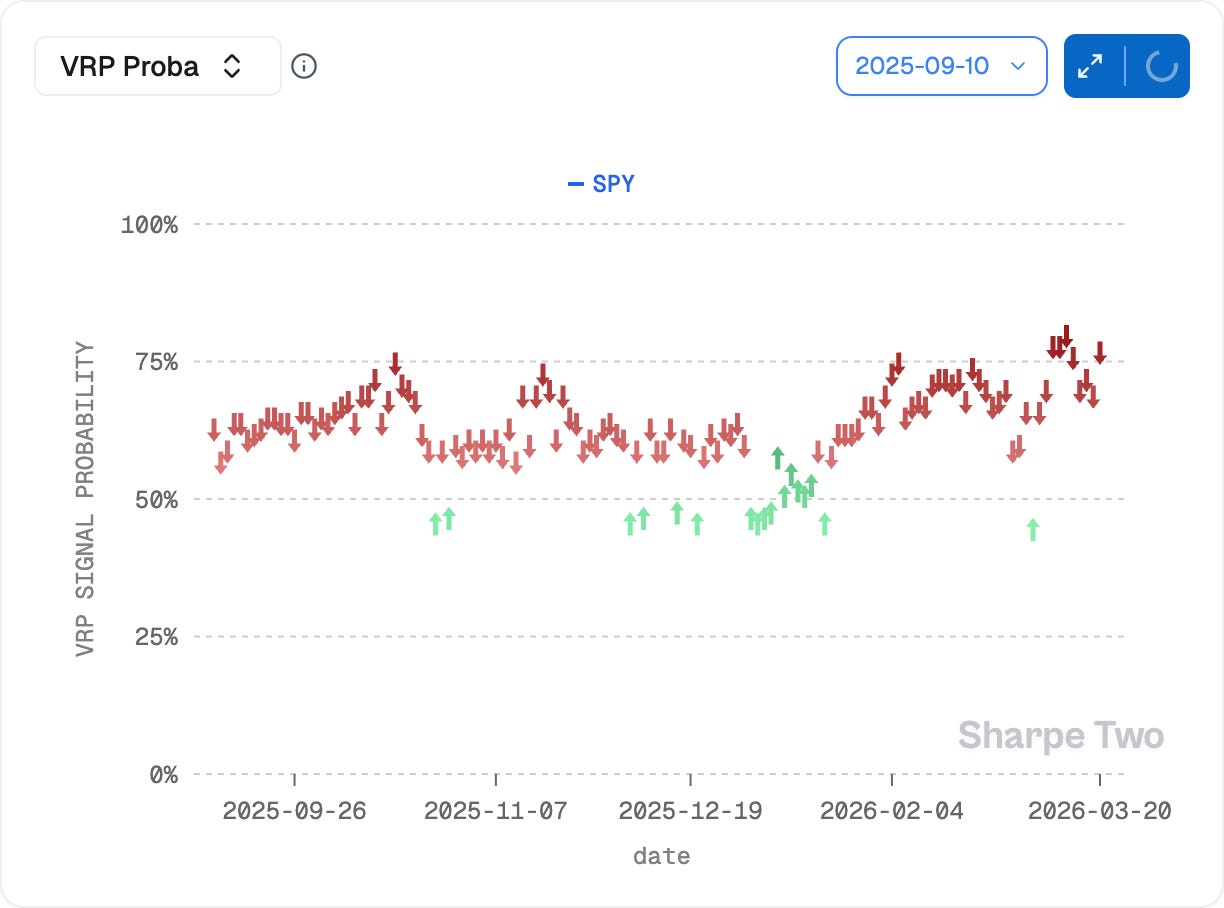

Our models are still showing some really strong probabilities that realized volatility over the next 30 days will come in below the implied volatility you can currently sell in stocks and bonds (above 75% is genuinely good), but the extreme left-tail nature of the current situation, and its abnormally higher probability of materializing compared to normal circumstances, cannot be ignored. The last time we saw 75% odds in SPY was in October and November last year and at the time the market was reacting to the AI thesis, a much more benign topic than the prospect of world powers casually throwing missiles at one another while the Strait of Hormuz is in a deadlock.

So we will conclude similarly than the last few weeks: do not try to be a hero. Hedge first, and if really you have some dry powder for market maneuvers, you can bet that until proven otherwise, nothing will actually happen. Hope is not a strategy, yet we can still hope that the different politicians will make the best decisions for the rest of the planet.

In other news

It was a Jay Powell on the defensive that we saw on Wednesday, justifying the latest dot plot presented at the March FOMC. Rates stayed at 3.5% to 3.75%, the dot plot still signals one cut in 2026, and Powell made it clear the Fed will remain “data dependent.” Fair enough, but the data is getting ugly is now the main modjo in the marketplace.

At the back of that iranian conflict which has already inflated oil prices by a solid 20% and is almost guaranteed now to be reflected in a wide range of product. Already the gallon of gas was reaching pretty hefty prices in the US, and one of the largest penury of pesticides, stuck in the Strait of Hormuz, may cause a rise in food prices around the globe.

Powell refused to pronounce the word “stagflation,” pointing to the fact that when it last happened almost 50 years ago, unemployment was in double digits and inflation was sky-high. And while we usually agree with him more than with the journalists in the room, the prospect of rising unemployment fuelled by AI optimization is something to keep an eye on, no? Powell is too smart not to think about this. But that may no longer be his problem: this was his penultimate FOMC as chair, while the handover to Kevin Warsh remains stuck, somewhere between a DOJ investigation and a Senate that refuses to confirm until the probe is over. In case this wasn’t settled by mid May, Powell would assure the interim. Joy !

Thank you for staying with us until the end. As usual, here are a couple of good reads from last week:

GPU obsolescence is complicated as explained in this very detailed artice. The debate about whether GPUs depreciate in 2 years or 6 misses the point: chips experience three distinct obsolescence curves, from training to inference to long-tail compute, and each follows its own timeline. A great framework for anyone trying to value AI infrastructure beyond the usual bull/bear binary.

We are constantly working on the next iteration of the app when we are not trading, and we obviously do it in an agentic way. Stay tuned for more announcements regarding our product, but in the meantime, here is a great article about leveraging the full power of agentic workflows.

That is it for us this week, we wish you a (mean reverting) week, and in the meantime, happy trading.

Ksander