Forward Note - 20260621

On the road to another lazy summer...

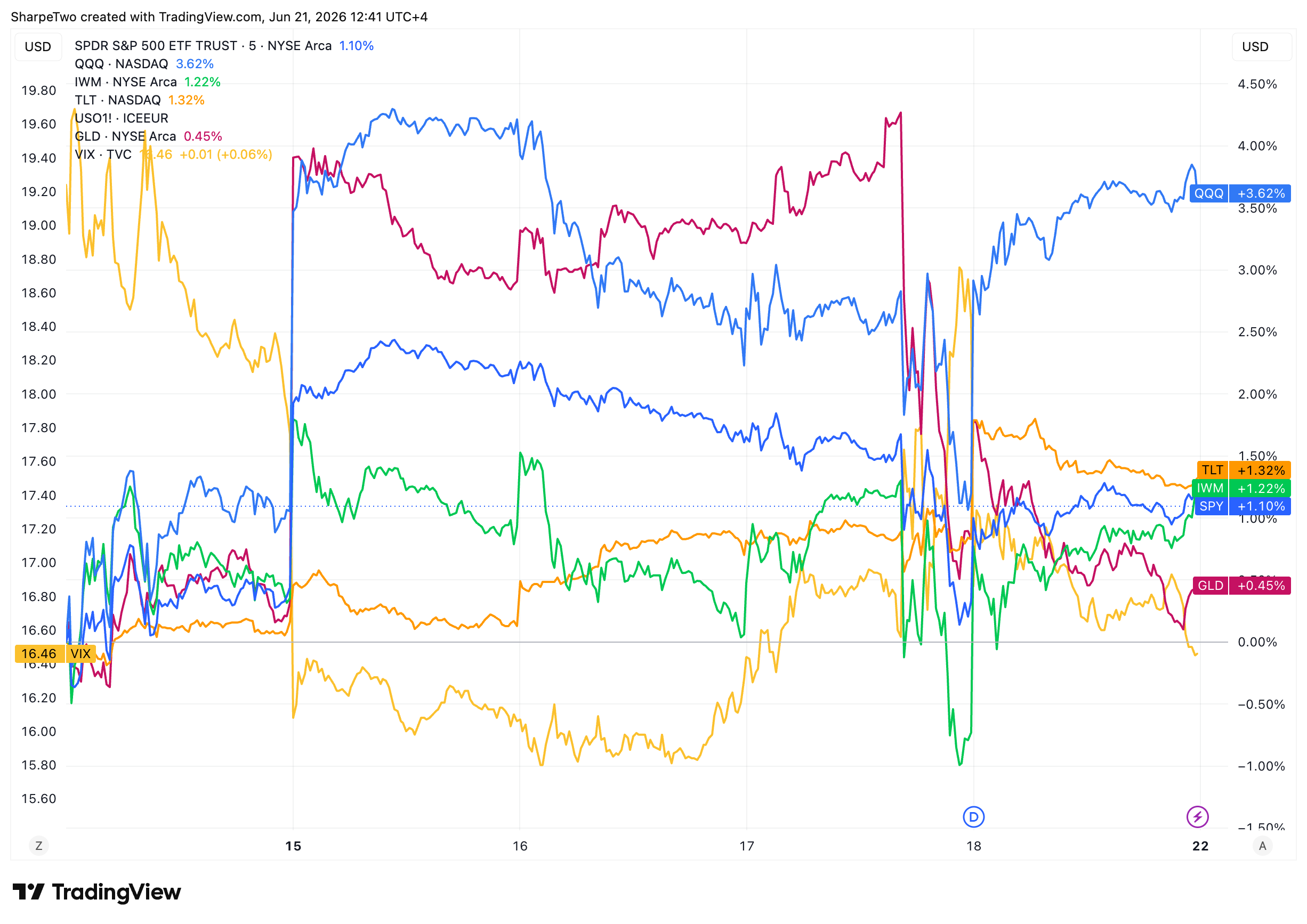

A busy period with more or less volatility, and in the end, equities are always up. This could easily be a line taught in any investment club or business school, and it has characterized the market since the Great Financial Crisis. And this one was no exception: the S&P 500 went up a little bit more than 1% while the tech-heavy Nasdaq added more than 3%. Year to date, and despite some pretty tense moments in 2026, the S&P 500 is up almost 10%, while the Nasdaq … 21%!

While we are still a few points away from an all-time high, the new Chairman, Warsh, inherited a market accustomed to setting fresh records rather than stagnating, and it will be interesting to see what kind of market he leaves behind four years from now. Especially because, as he chaired his first FOMC last week, he already marked a stark contrast with his predecessor, Jay Powell. Warsh has never hidden that he doesn’t believe in forward guidance, and that, to him, the best economist is the market, so (central) bankers should be taking their information from it rather than feeding information to it.

And that was exactly what he did: a pretty slim statement to announce that rates would be on hold, and a pretty short press conference to comment on the decision. Time will tell whether he adapts his style to the market over time, or the other way around. What is for certain is that, after a rocky session on the back of a “hawkish” (really?) press conference, the market recovered to finish on the highs of the week. Was it a free pass? Do they truly not care? It’s the beginning of what promises to be yet another lazy summer, and we wouldn’t draw conclusions too quickly: the first big test for Warsh will be in August, at Jackson Hole.

In the meantime… VIX 16 … tells you everything you need to know! Yet a few things will have to be verified over the next week or so before we officially start the traditional cruise toward July 4th. First of all, we left realized volatility at a weekly high last week, and while things have quieted down, it was still pretty shaky.

The market initially reacted pretty poorly to the remarks from Warsh before reversing most of the losses the day after. This was also the end of the quarter and the half-year, and it is not unlikely to see “weird” moves and acute volatility in that period. So was it really Warsh? Was Warsh an excuse for portfolio readjustment? The truth is often pretty blurry, and we would be careful with any direct causal explanation at this time of year.

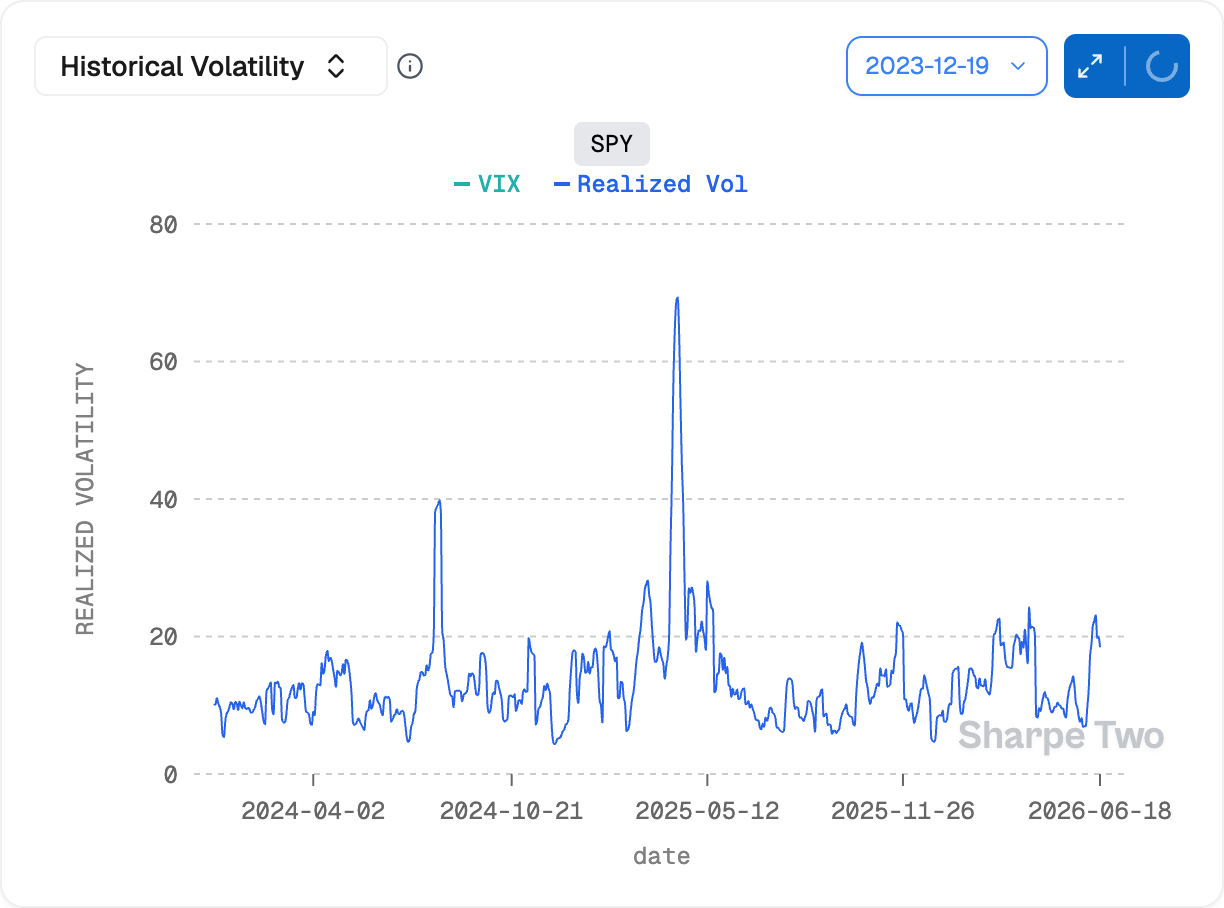

What is for certain is that we still forecast realized volatility to come down a bit from what we observed over the last two weeks:

From 20% to 15%, and it will be interesting to see on Monday whether some volatility is left, or whether we open the door to coming back down to 12 much faster than this chart currently anticipates. With the Iran situation cooling off for good and no major new numbers on the horizon, the catalysts may be a little hard to find to keep the swings we’ve seen going. Yet until proven otherwise, the first few weeks are not the best for options sellers:

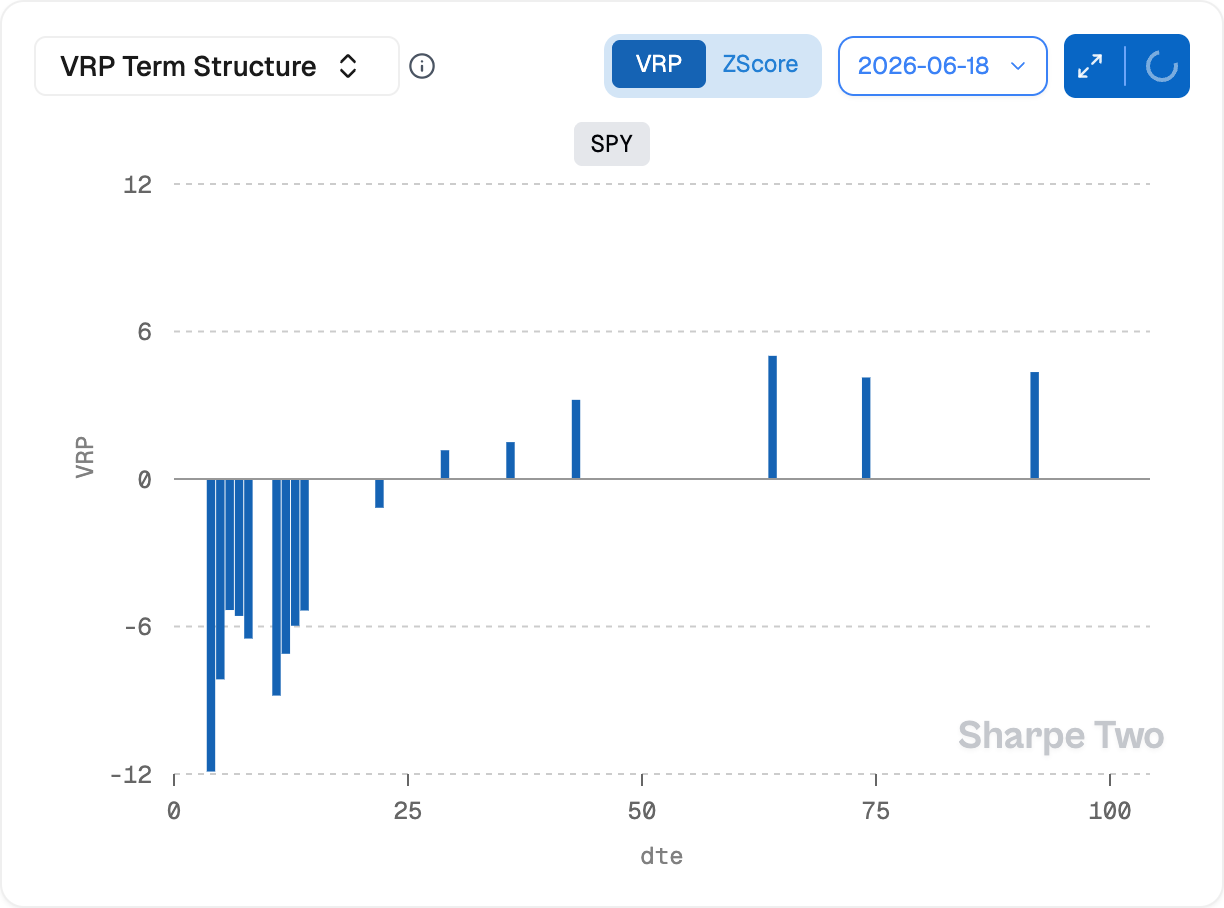

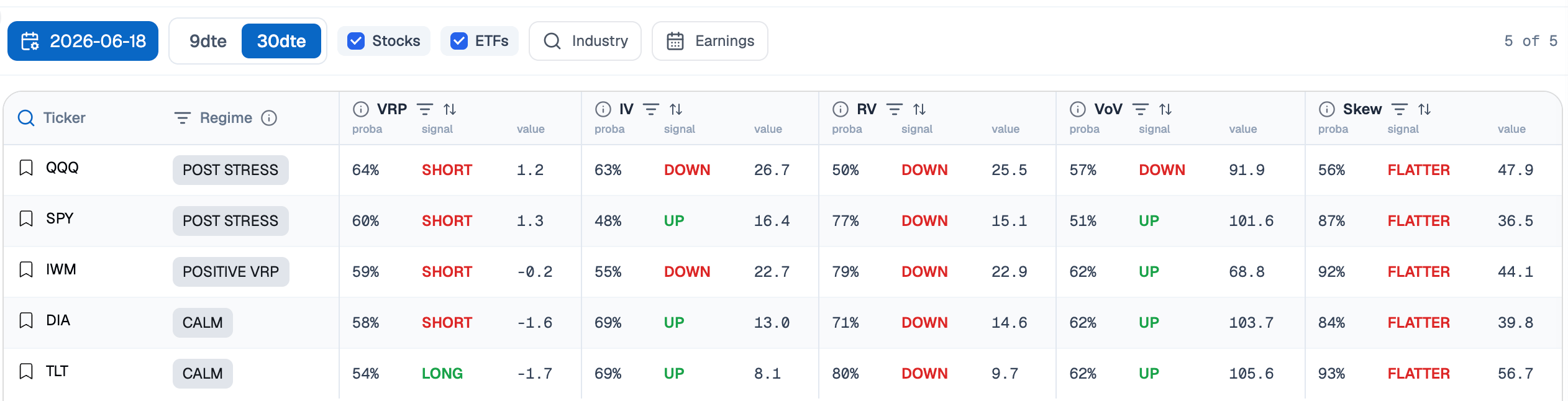

We were already writing last week to be careful with short-dated options, and the swings over the last week proved us right. If you were patient, you found some situations, especially in the wake of the Warsh conference, where selling vol was a better bet from a VRP perspective than it was at the close on Thursday: less than 2 points at around 30 days starts to be pretty slim. Obviously, if subsequent realized volatility turned out to be 8, that would be a hell of a trade. At the moment, our signals show that the implied volatility you sold today has about a 60% chance of exceeding the subsequent realized volatility. While that is not completely flip-of-a-coin territory, it should push you to consider something else. If you really want to trade equities, a Nasdaq 20-delta strangle presents much better odds at the moment.

However, for all of them except the Nasdaq, we currently anticipate the skew to flatten a bit, which means puts repricing favorably relative to calls. This aligns with a regime where we anticipate realized volatility cooling down overall. Yet another sign that if you are extremely bearish, you may want to reconsider your thesis. We are not at a point of real worry in the marketplace: yes, we know the financial media will insist on the shaky situation with Iran, or potentially inflation, but that is not where the market’s focus is at the moment.

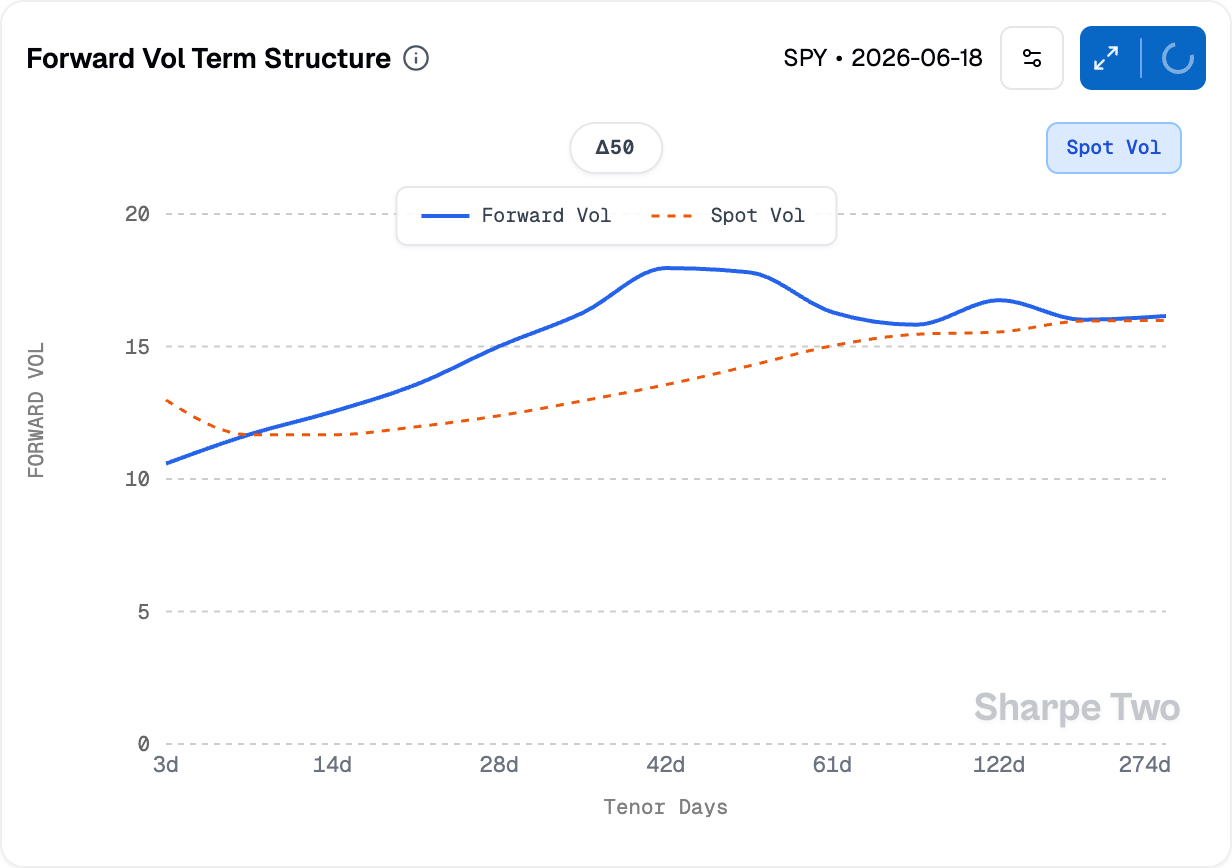

When looking at the forward volatility term structure, the next bump in the curve is scheduled for the next FOMC week at the end of July. Therefore, let us hope for a truly boring market in early July so we can enjoy a few days off, and let’s see what the second half of the year has in store for us.

In other news

How hawkish was Kevin Warsh exactly? Some people will talk about this much more eloquently than us. However, what is interesting is the slight contradiction currently playing out. The dollar is arguably getting stronger over the last few weeks on the back of constant talk of a Fed hike, while bonds are… getting slightly more expensive, with rates giving back some of the gains they made a month ago when Powell was leaving the Fed.

In normal circumstances, we would say that one of them is lying and the situation may correct itself. But can we really say that we are in normal circumstances? Let’s take a concrete example: oil is finally back at its pre-crisis level, well below $80 a barrel, down from $120 a barrel no more than a couple of months ago. Yet there has been no sell-off in emerging market currencies, in particular the ones heavily dependent on oil like India and the Philippines, and no major sell-off in riskier assets overall: none of the stock markets worldwide went through hell on the back of a truly disruptive situation. In fact, on some interesting occasions, they went up like crazy (Korea). So why is that? We definitely do not have the answer, and it is interesting to watch economists scratch their heads to explain what is a blatant contradiction of every economic textbook.

Another proof, if needed, of the weak relationship between the economy and the market’s behavior. The lesson? Always the same: be careful with what is for certain. The odds that it doesn’t happen are always underestimated.

Thank you for staying with us until the end. As usual, here are two great reads from last week:

A year and a half after the release of the MCP protocol, you are starting to see a much deeper integration between merchants and consumers through … agentic pipelines. And while the idea of having agents purchase things for us looks like a slam dunk, this article actually questions that. If you are building an agentic business at the moment, this is worth a read.

We haven’t talked about prediction markets in a little while, but that doesn’t mean they are going away. In fact, they may only be hardening themselves to become stronger. A big problem for customers over the last few months has been ghost fills, a phenomenon that could be characterized as the reverse of the early-2000s experience at the beginning of HFT. You thought you had a trade on… only to discover that it was never registered on chain. Here is an interesting paper explaining and quantifying the case in detail.

That is it for us this week. We wish you a great week ahead and, as usual, happy trading.

Ksander