Forward Note - 20260531

Have you noticed?

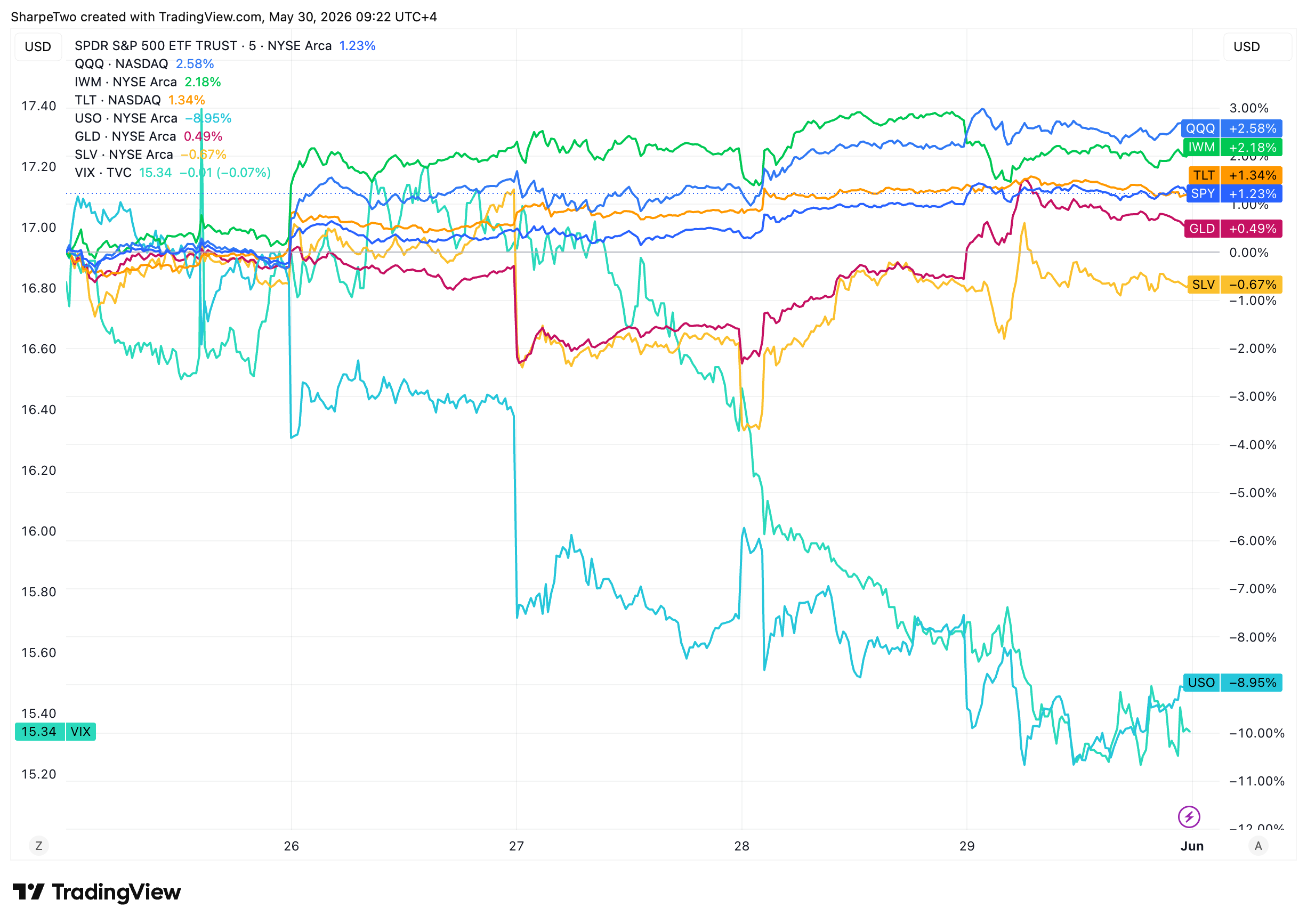

Despite all the gesticulation last weekend, the end of the world didn’t happen and the promised firework for Memorial Day will just stand as yet another unfulfilled fantasy in the shallow memory of social media. As a consequence, by many regards, the week was fairly boring: stocks went up again, to fresh all time highs, with the S&P 500 adding a little less than 1.5% and the Nasdaq a little more than 2.5%. Rates relaxed, and oil lost almost 10%.

Why is that? Because for the first time since the back-and-forth, almost public negotiation between Iran and the US, Iran confirmed on Wednesday that a deal was in the making, a material step in the right direction after months of open trolling of the US administration, claiming at times that President Trump was talking to himself.

The deal of course includes a reopening of the Strait of Hormuz, and, more surprisingly, a $300 billion fund invested worldwide for the reconstruction of Iran. We won’t comment on who won and who lost in that deal; that is far beyond our pay grade. We will just point out that, despite the market reaction, many are still convinced we are not out of the woods.

And why should we blame them? It has been going on like this for months, so why not an extra few months? First of all, because this is the first time since the beginning of the war that oil closed meaningfully down two weeks in a row: -5% last week, and now -8%. Once again, the market is a formidable machine at aggregating information. It is slightly imperfect, yes, but not meaningfully enough to say that, on average, an event priced at 10% was actually a 25%. And if risk perception is going down — whoever the next social media Cassandra may be — the market firmly disagrees right now.

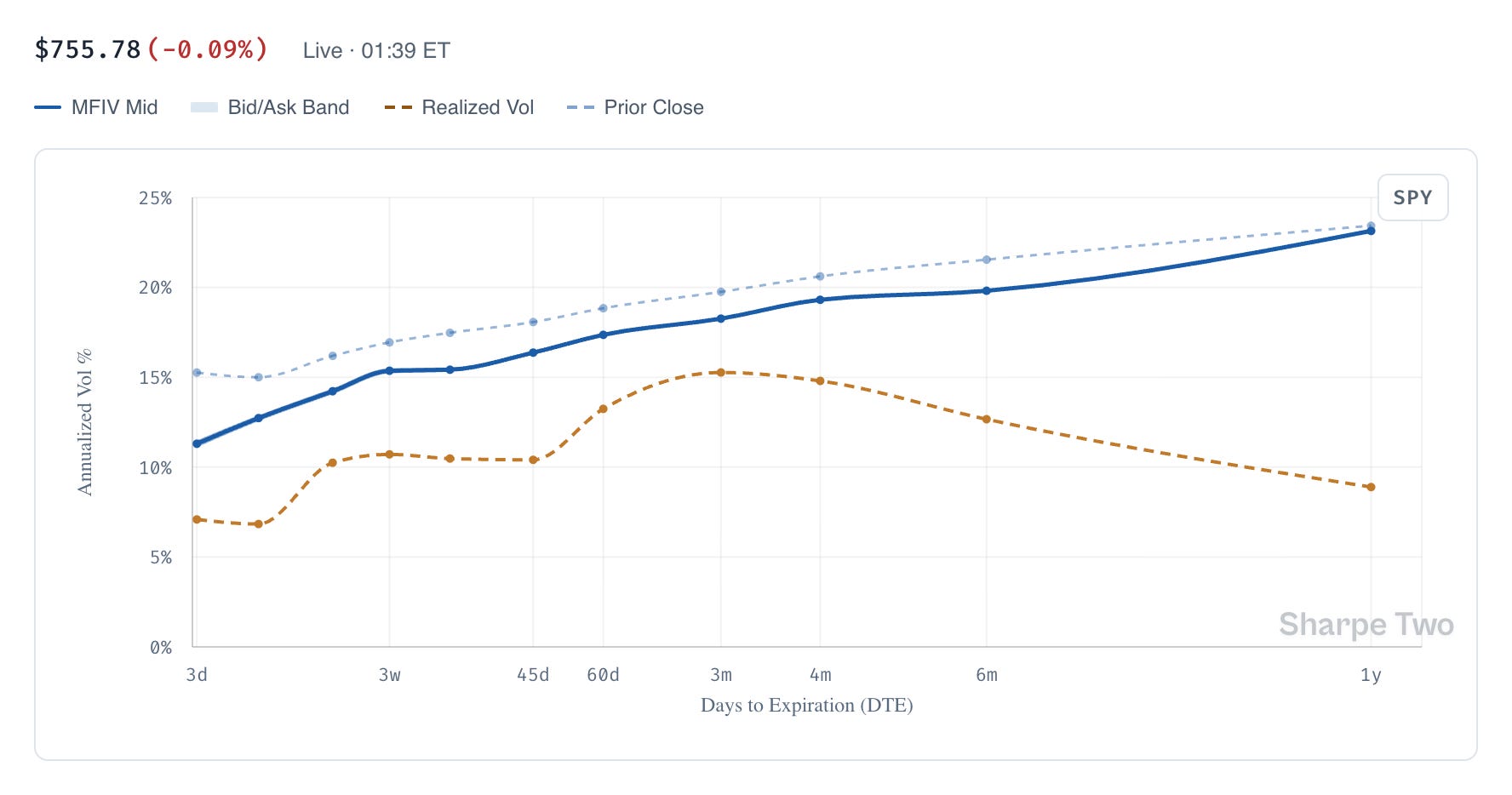

And there have been many little signs like this, have you noticed? Let’s start with the obvious one - VIX on the 15 handle. This is genuinely the lowest level observed since early January, where a surprise attack on Venezuela was in fact just the early sign of what the rest of Q1 would look like. Is VIX too low? Once again, that may be your opinion, but as it stands, it is still materially above realized volatility.

Five points of VRP when the jump risk in equities gets meaningfully lower (realized volatility flirting with 10) is a genuinely good and much more stable condition for harvesting than the quite stressful weeks we had at the end of March — which feels like a lifetime ago now.

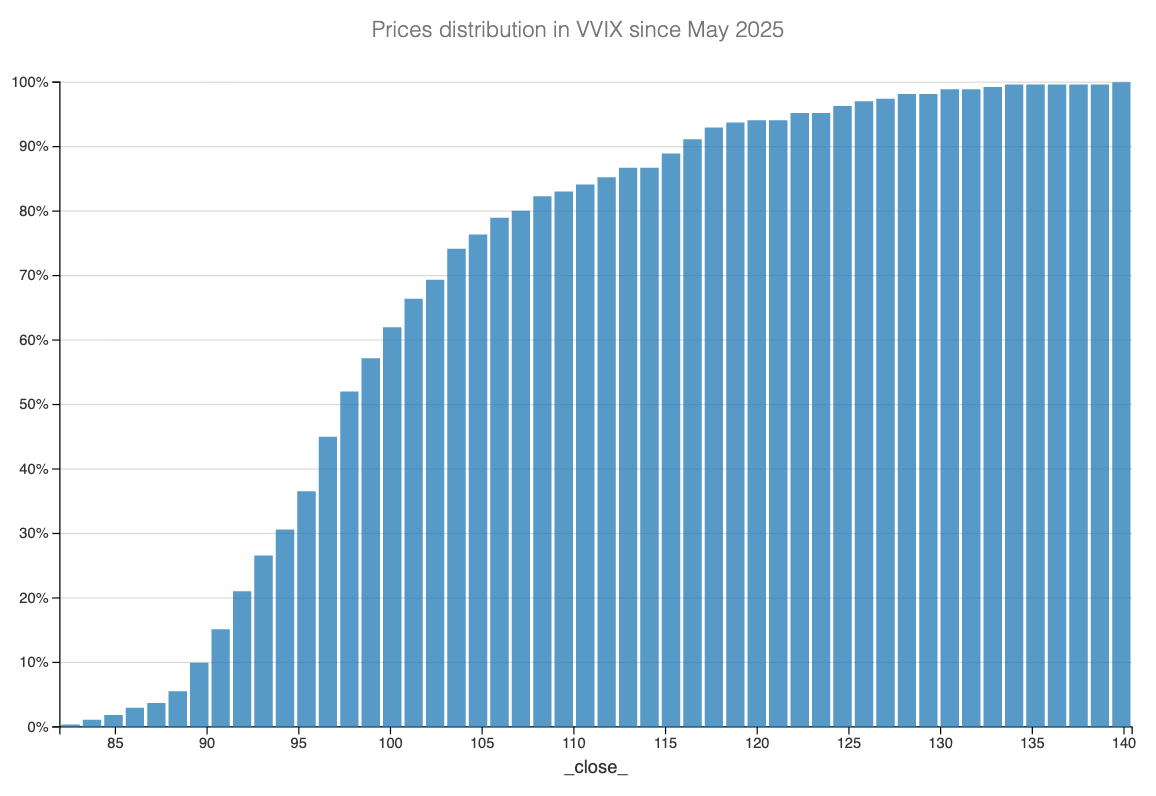

Yet we’ve been yapping about VRP for weeks now, so an astute reader could just say: okay Ksander, is that all you got? No, we have more. Once again, we don’t know if you’ve noticed, but VVIX is materially below its long-term average observed over the last 12 months. In fact, VVIX is so low that it is digging in the lowest percentiles observed since Liberation Day.

VVIX, or the implied volatility contained in VIX options, tells you the market’s expectations for VIX movement over the next 30 days. Last week it closed at 90, which was already the lowest level observed over the last 12 months and also happens to be its long-term average. Now it is at 85, one of the lowest readings recorded over the last year.

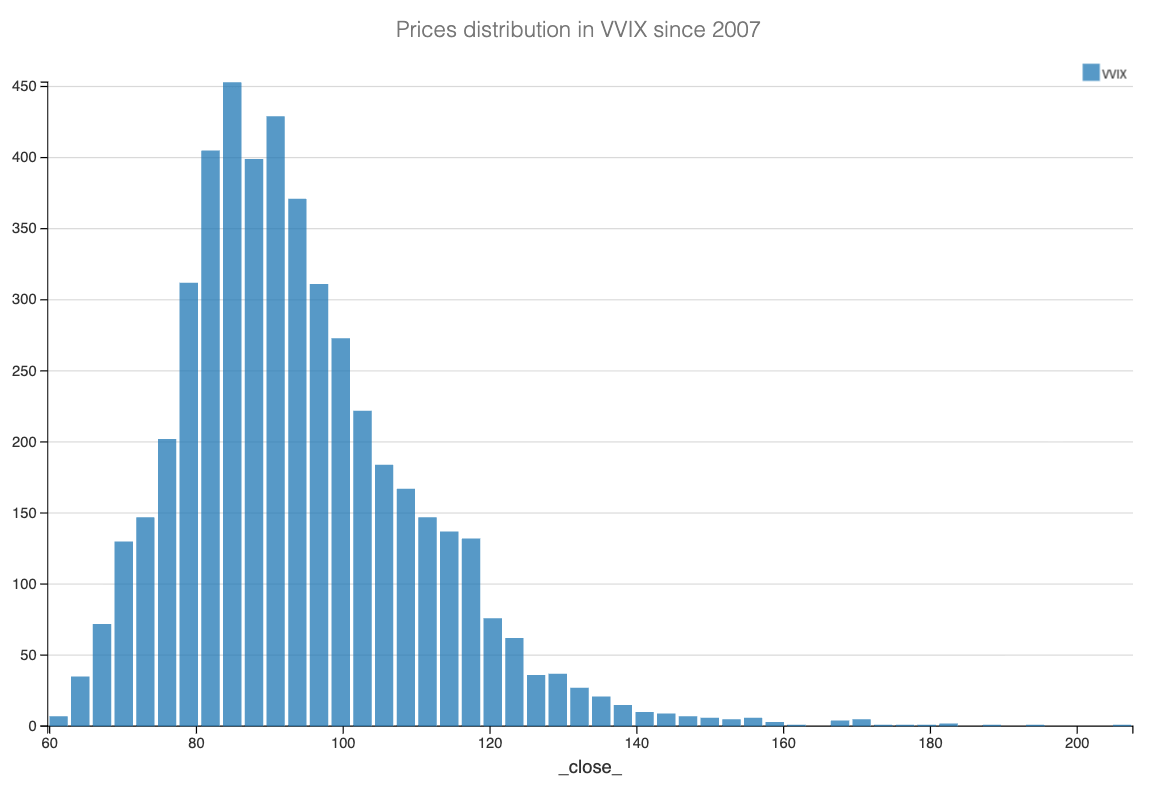

For many, this will be yet another sign that the market is completely dumb, out of whack, manipulated — whichever qualifier you may want to use. But it really is not. First of all, because a reading of 85 in VVIX, in the grand scheme of things, is really not that abnormal.

So essentially, in a matter of just a few weeks, the marketplace decided to stop buying these arguably most expensive insurance contracts. That points in one direction: risk perception is shifting. And that may genuinely be for good reasons.

With the Iranian war “out of the way,” the immediate catalysts for markets going down are off the menu. You would need something genuinely new and unexpected to rattle the markets. In other words, nothing in the current chatter of the day is representative anymore: it is all priced in.

And with summer now just a few weeks away, one has to squint really hard to find a reason why we would exit this quiet regime any time soon. The first FOMC under Warsh in mid-June? Likely a market mover, but we will have to wait and see if it turns out to be a true disruptor. How about inflation, the AI bubble, etc.? VIX 15 tells you everything you need to know: they may be an issue eventually, but not in the next 30 days. Lastly, we don’t know if you’ve noticed, but the market is clearly gearing up for some astronomical IPOs to land soonish.

Human beings are a paradox: when things are quiet we want movement, and when there is movement we want quiet. We forget the bad of one regime and fantasize about something new, something different. Be careful what you wish for. We don’t mind calm and boring — in fact, we crave it... as long as the market keeps baking in a healthy Trump Risk Premium. And while we won’t lose any sleep over a VVIX at 85, we will monitor closely to see whether these 4 to 7 points of VRP — observed consistently for more than a year in US equities — will erode, and with them, some of the fantastic sources of edge we’ve had at our disposal.

In other news

The biggest story of the week, by a wide margin, was the leak of the draft US–Iran agreement and the rather eye-watering price tag attached to it. According to The New York Times via multiple wires, the proposal floats a $300 billion “international investment fund” to rebuild Iran, paired with a 60-day ceasefire, a commitment to keep the Strait of Hormuz unrestricted, and even a Lebanon clause aimed at calming Hezbollah. The architects, reportedly Steve Witkoff and Jared Kushner, even floated joint ventures between US energy majors and Tehran’s oil sector.

For context, $300 billion is roughly the GDP of Finland and a good chunk larger than the entire Marshall Plan in today’s dollars. Whether any of this lands intact is another question entirely — Trump has not signed, the two sides still disagree on who controls the strait, and Iran wants its $24 billion in frozen assets released up front. But the symbolic shift is real. For markets, the message is simple: the geopolitical apocalypse the VIX was pricing in March has, for now, been swapped for a deal — and an oil chart down 10% on the week.

Thank you for staying with us until the end. As usual, here are two good reads from last week:

Here is an extraordinary read about crypto market, edge and making big (big) money while you can. And even if that source of edge is now gone and impossible to extract, it should give you some ideas about where to look for places where you have asymmetry of information and not a lot of competitor. Spoiler alert: not in 0 dte.

If you still do not know what a perp is, you still have a few weeks to catch up. Here is an article from the FT talking about their raise in popularity and why the convergence between tradeFi and defi may be closer than one was originally thinking.

That is it for us this week. We wish you an excellent NFP week, and as usual, happy trading.

Ksander