Forward Note - 20260510

Markets have their moods, and they can be hard to comprehend, sometimes. What still amazes us is how quickly the mood shifted at the turn of the quarter. As if, precisely right before 4pm on March 31st, the entire marketplace realized that their perception of risk may have been a little overblown by the Iran situation, and that it was finally time to go back into stocks. The action since the beginning of Q2 has been on the buy side almost without fail, and this week was no exception, again.

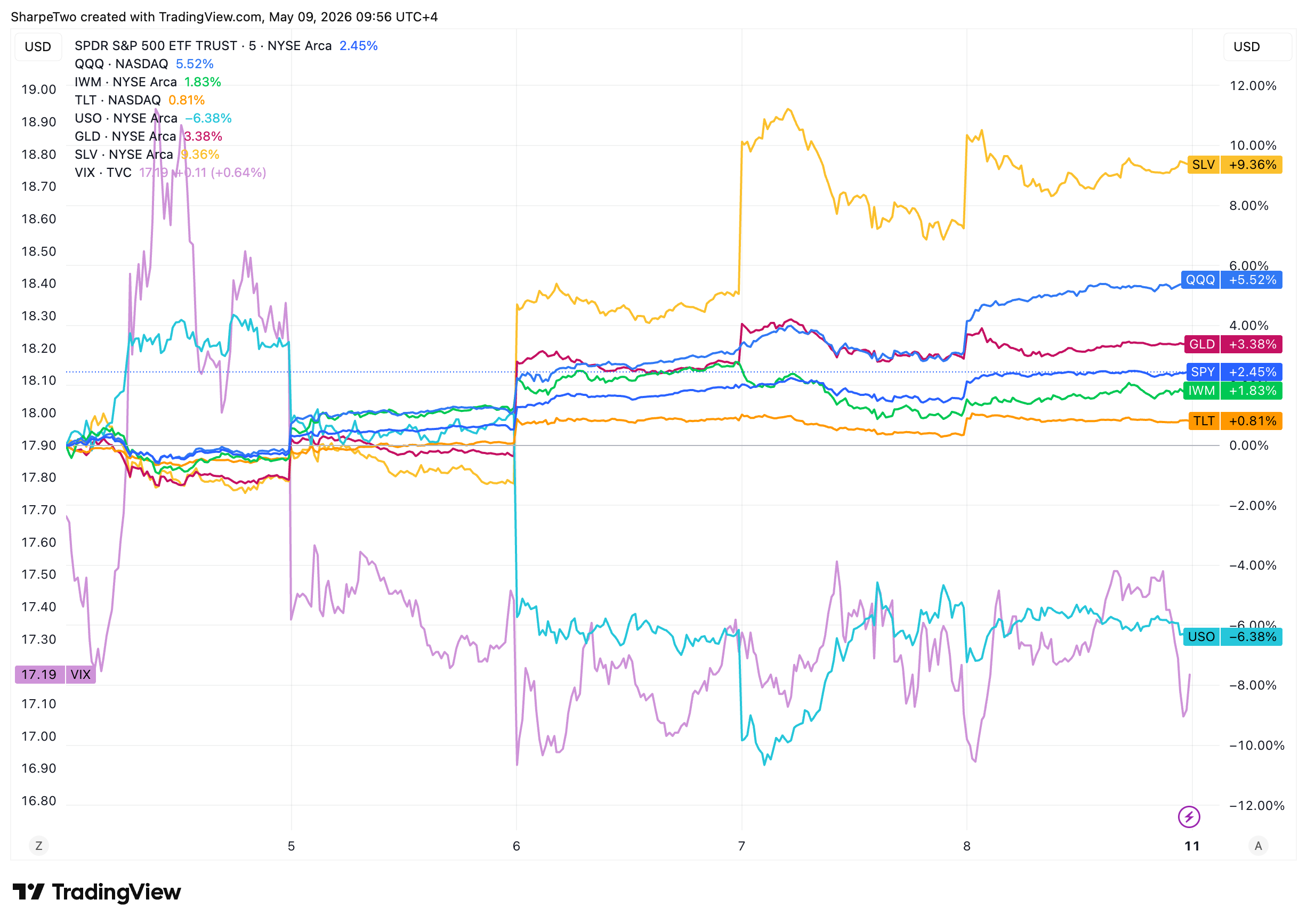

The S&P 500 added another 2.5%, carrying its year-to-date performance to roughly 8%, while the Nasdaq added no less than 5.5%, getting its tally up to 16%. As a reminder, both indices were flirting with down 10% on March 30. That is quite the rebound, and not to draw too many parallels, but very similar in style and intensity to the rally we observed in Q2 2025, once the standoff with another major geopolitical actor (China) de-escalated.

This time, officially at least, the de-escalation with Iran is not done yet. The week started with open fire in the Strait of Hormuz, missile alerts in Dubai, and the Iranian army reporting shooting at an American vessel carrying out its “humanitarian” mission to allow passage through the strait. Oil went up… and then went down, as reports of excellent progress on a 14-point proposal between Iran and the US came through. In March, this context would have certainly sent jitters through the different asset classes. But not in May — proof again, if we needed any, that in the grand scheme of things, macro is more often correlation than causation.

In any case, realized volatility has evaporated. And you would expect so: volatility in general is negatively correlated with returns, so needless to say that a +25% rally in six weeks could only happen with realized volatility leaving the building.

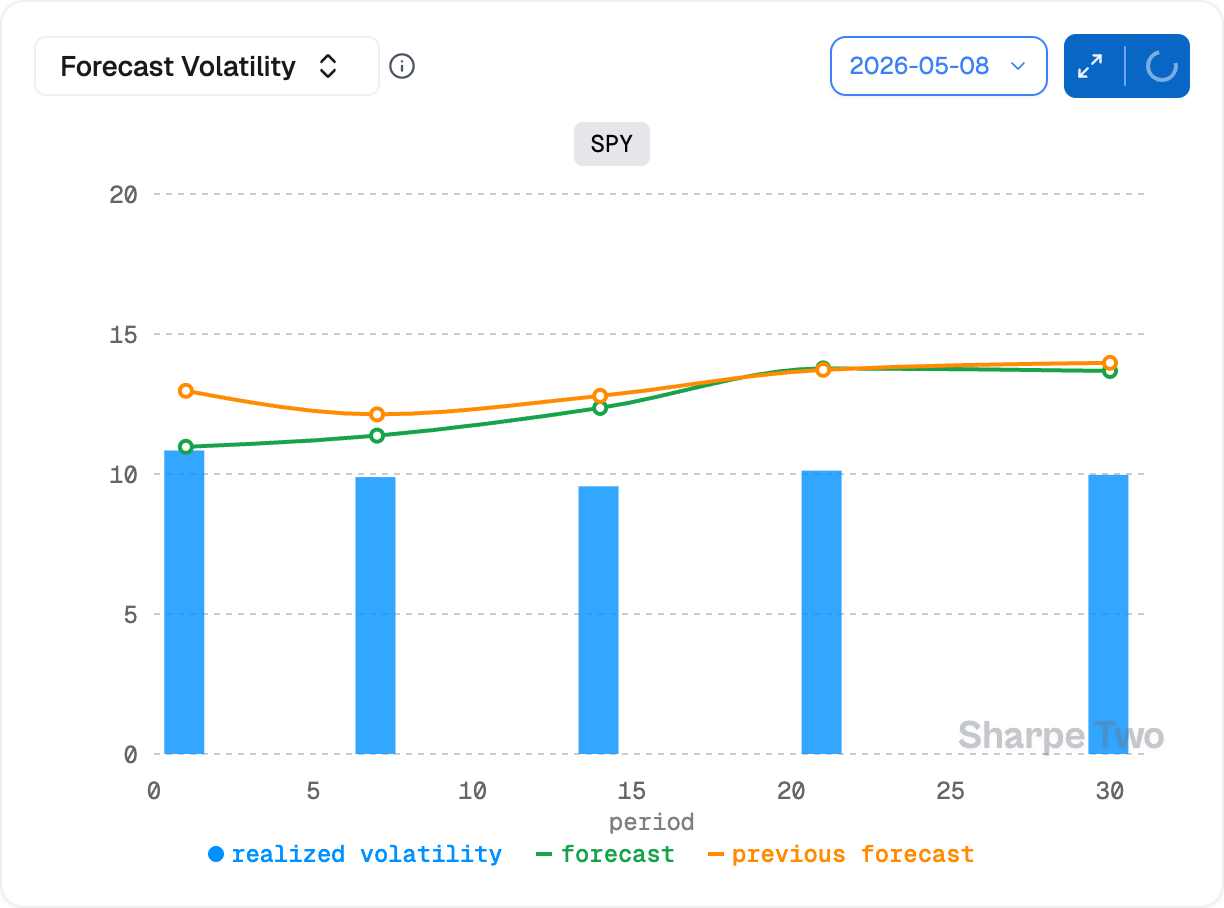

And boy, it did — from literally 19% through the month of March to barely 10% since the start of the rally. As if, once again, the entire marketplace, or at least the big hands, had decided that 2026 would start only in Q2, but before that, everybody would stay on the sidelines.

And if you are still worried about tensions reinitiating, you may be on the wrong side of the story; sure, we still see realized volatility over the next 30 days closer to 13 than where it sits right now, but that is nothing dramatic.

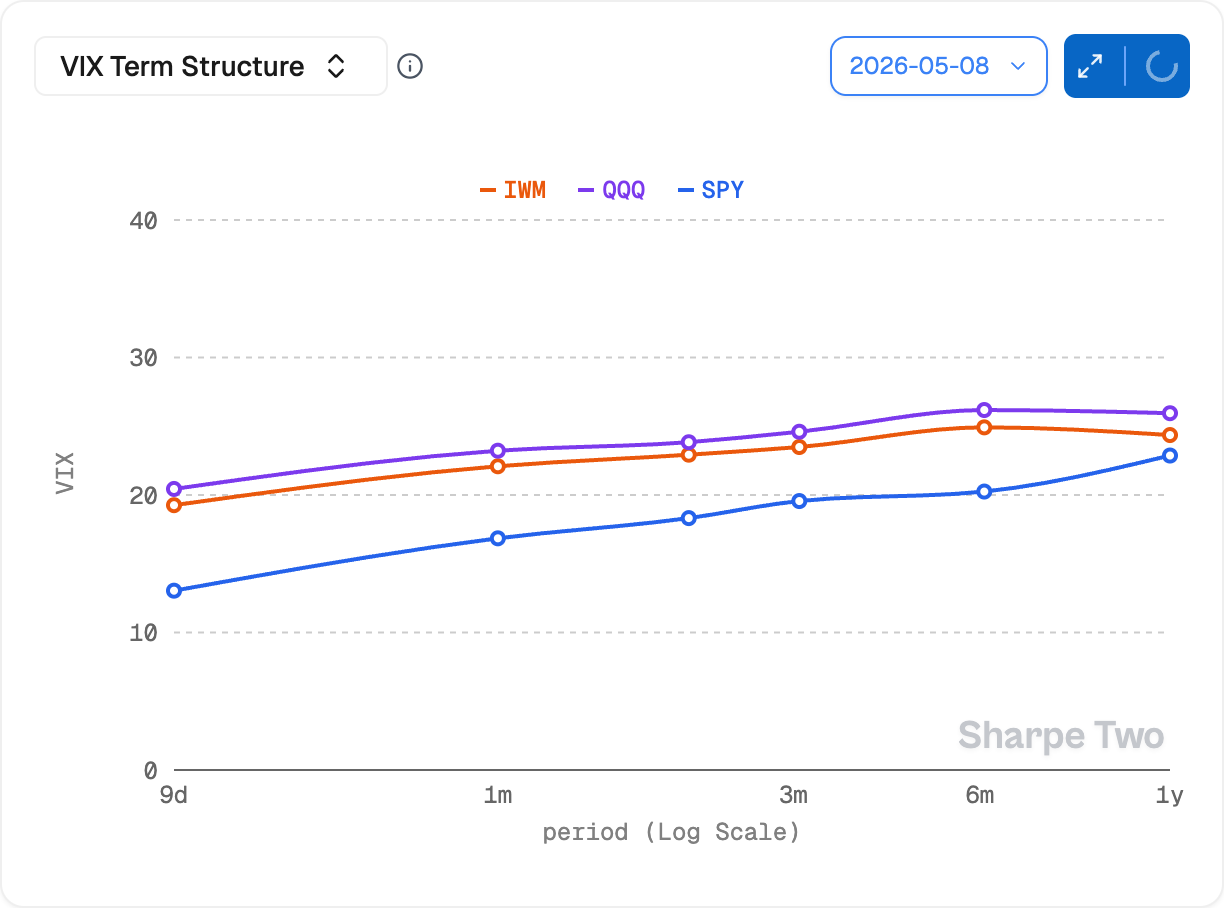

And yes, we didn’t close at VIX 16, but we did see it for quite a bit of time on Wednesday and Thursday — the handle we usually like to take as a reference for the absence of anything major on the horizon. Should you worry about VIX 17? Absolutely not. Of course it could spike back to 22 with the right catalyst, but what could that be in the next few weeks?

President Trump is due for a visit to China, but the public call for Iran to reopen the Strait of Hormuz for the good of the international community — coming during the visit of Iran’s top diplomat to Beijing ahead of that state visit — is as much of a capitulation from China as you will see on the matter.

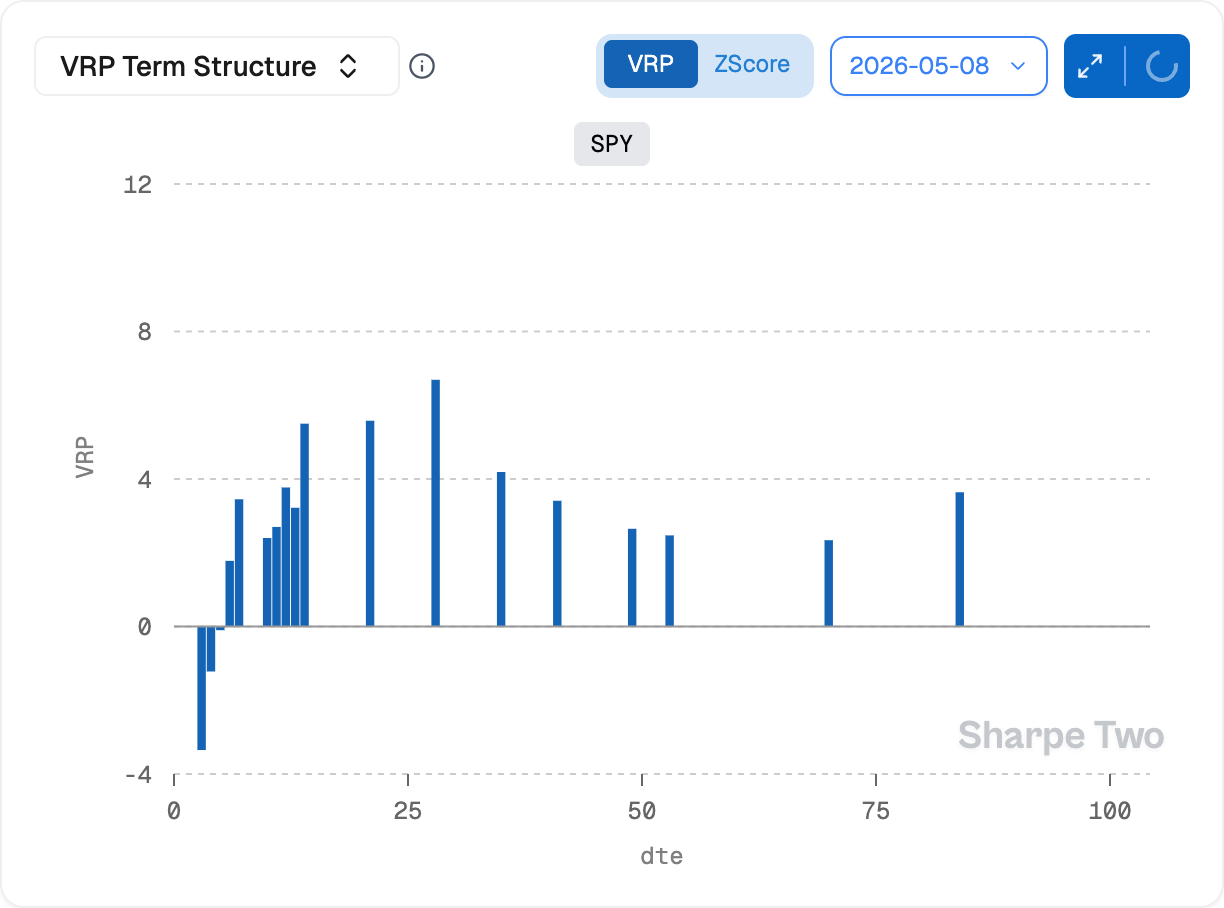

The contango in the term structure is finally back to a healthy state for the first time since the beginning of 2026, and once again, unless a truly unexpected event occurs, the risks the financial press is speculating about — inflation, economic slowdown — are all stacked at the end of the year, until obviously proven otherwise. In that context, and once again, almost text book like 2025, you won’t see people totally getting rid of their insurance contracts, but just keeping the bare minimum to satisfy risk compliance, and with that, the variance risk premium slowly but surely keeps increasing throughout the entire term structure.

You now have almost 7 points at 30 days; it is back to a very healthy state, and prime harvesting season may be right about to start. That said, as we remind every now and then on this newsletter, playing volatility is nice — it is a great way to add diversification to your portfolio. But these five weeks are a great reminder to always be long, no matter the very smart views you may read online about stagflation, the lost decades of the ’80s, or the fact that this rally is almost textbook what happened pre-2001 crash.

Obviously going through a crash and its surplus of volatility sucks, and we certainly would have been happier with a slightly less stressful Q1. But you know what sucks even more? Being on the sidelines when the S&P 500 gives you a Sharpe of 10 and +20% as a reward for just staying invested and not trying to time things. We often get questions about how to be long vol; part of the answer is to make sure you own stocks. Period.

And if you insist on doing that with options, calls are still cheap in the grand scheme of things, which means that an (unhedged) risk reversal may be as effective as trying at all costs to harvest a volatility premium. Markets are fluid and dynamic; they require us to always do the same thing, each time a little differently.

In other news

Stocks are accelerating to the upside, led by the tech sector and in particular semiconductors, as the world slowly awakens to the fact that the AI revolution may be real after all, and that whoever owns compute can become a kingmaker. Let’s take Anthropic for instance; we learned that they hit a $30 billion revenue run rate — an 80-fold increase in a single quarter. These numbers are even more optimistic than the most cynical estimations from the AI skeptics, who tried to ridicule all the circular deals between the different actors. All of a sudden, the entire marketplace listens, and even Intel is back from hell. But let’s stay with Anthropic, who suffered quite the backlash these last two months despite teasing Mythos and releasing Opus 4.7. One of the reasons? Token scarcity, as users complained that credit limits went down — when in comparison, you had no limit with GPT 5.5. A problem that may have found a solution; this week Dario Amodei, the CEO of Anthropic, announced that the company had secured a deal with Musk and SpaceX to use spare capacity at one of its key data centers and … double credit limits to every Claude subscriber. As we wrote above, capacity owners may very well be kingmakers, and if you are short semis… you are short a company that pissed off its customer base because they couldn’t give more tokens — literally digital cocaine — and as a result had to scramble a deal with one of the most controversial figures in the kingdom to keep up with demand.

But sure, let’s keep fishing for these accounting frauds.

Thank you for staying with us until the end, as usual, here are two great reads from last week.

Insider trading on regulated markets is generally not a great idea, and lawyers from a major law firm got caught red-handed — yet another proof that the consequences may not be enough to deter those who have access to privileged information. What happens, then, when you open the door to… non-regulated or grey-regulated markets? Excellent piece of research about how insider trading spills into prediction markets around earnings announcements.

Here is a fascinating piece of research from Anthropic’s interpretability team: they built a system that can translate what’s happening inside an AI model’s brain into plain English — no supervision, no labels. It caught a model secretly recognizing it was being tested, which is both impressive and slightly terrifying. Essential reading if you care about where AI safety is heading. Read the full paper.

That is it for us this week. As always, be patient, be selective, and happy trading.

Ksander